Portfolio News

Cyera + Oasis: Securing the AI-Native Enterprise

July 28, 2026

Portfolio News

Cyera + Oasis: Securing the AI-Native Enterprise

July 28, 2026

Portfolio News

Our Investment in Paper: The AI-Native Design Space

July 23, 2026

Portfolio News

Tackling Industrial AI’s Last Mile Problem: Our Investment in Arrakis

July 22, 2026

Portfolio News

Cognition Acquires TierZero: Building the Autonomous Engineering Agent

July 20, 2026

Portfolio News

Building the AI-Native Identity Operating System: Why We're Backing Oak

July 15, 2026

Portfolio News

Our Investment in Axle Energy: Turning Everyday Energy Devices into Grid-Scale Flexibility

July 8, 2026

Portfolio News

Leading Agave's Series A: AI Infrastructure for the Construction Industry

July 7, 2026

Portfolio News

The Device That Remembers So You Don’t Have To: Our Investment in Pocket

June 29, 2026

Portfolio News

Our investment in Tolmo: AI security agents with production context

June 18, 2026

Portfolio News

Our Investment in Twenty: Industrial-Scale Cyber Operations

June 17, 2026

Portfolio News

$1 Trillion of AI and Cloud Spend will Need to be Optimized: Our Investment in PointFive

June 8, 2026

Portfolio News

Cloudflare + VoidZero: The Next Chapter for JavaScript Tooling

June 4, 2026

Portfolio News

Unlocking the $4 trillion problem: continuing our partnership with OpenFX

June 3, 2026

Portfolio News

Our Investment in Perceptic: The AI Operating System for Drug Discovery and Development

May 26, 2026

Portfolio News

Welcome, Viktor: The AI Coworker for the Modern Workplace

May 19, 2026

Portfolio News

Fractile: The future of AI inference

May 15, 2026

Portfolio News

Building the Foundation for Modern Medicine: Our Series B Investment in Forus

May 12, 2026

Portfolio News

Our Investment In Ciridae: Serving the 99% of Businesses AI Has Left Behind

May 12, 2026

Portfolio News

Our Investment in Nova: Bringing Frontier Intelligence to Every Enterprise System

May 6, 2026

Portfolio News

Our Investment in RadixArk: Building the Open Infrastructure for AI

May 5, 2026

Accel News

Our latest fund: Early Insight and Enduring Partnership

April 14, 2026

Portfolio News

Our Investment in Legora: The Legal AI Operating System

March 30, 2026

Portfolio News

Powering the Agentic Economy: Our Seed Investment in Sapiom

February 6, 2026

Portfolio News

Partnering With Material Depot: Building Design-First Indian Homes

February 4, 2026

Portfolio News

Congratulations to Amagi on its IPO

January 20, 2026

Portfolio News

Accel Leads depthfirst’s Series A: Securing the World’s Software

January 14, 2026

Portfolio News

Graphite + Cursor: One Engineering Platform for the AI Era

December 19, 2025

Portfolio News

Port: The Platform For Engineering’s Agentic Future

December 11, 2025

Portfolio News

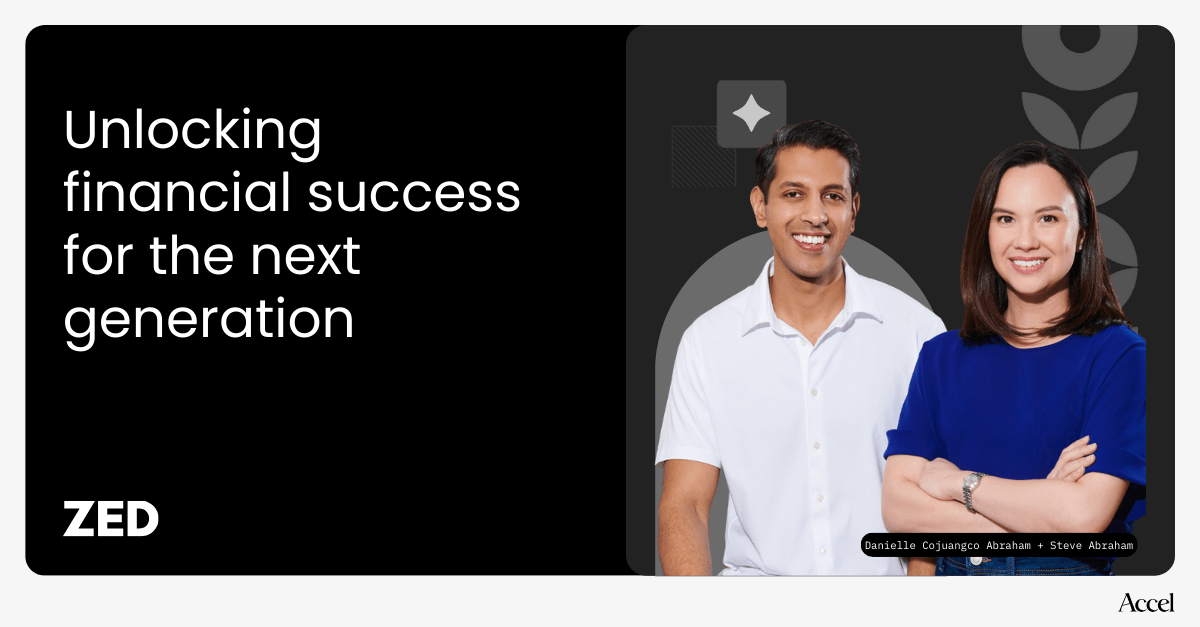

Accel leads Zed’s Series A: A Neobank for a New Generation

December 10, 2025

Portfolio News

Bracing for the Silver Tsunami: Our Seed Investment in Hera

December 9, 2025

Portfolio News

Our Series B in PermitFlow: Breaking the Construction Bottleneck with AI

December 2, 2025

Portfolio News

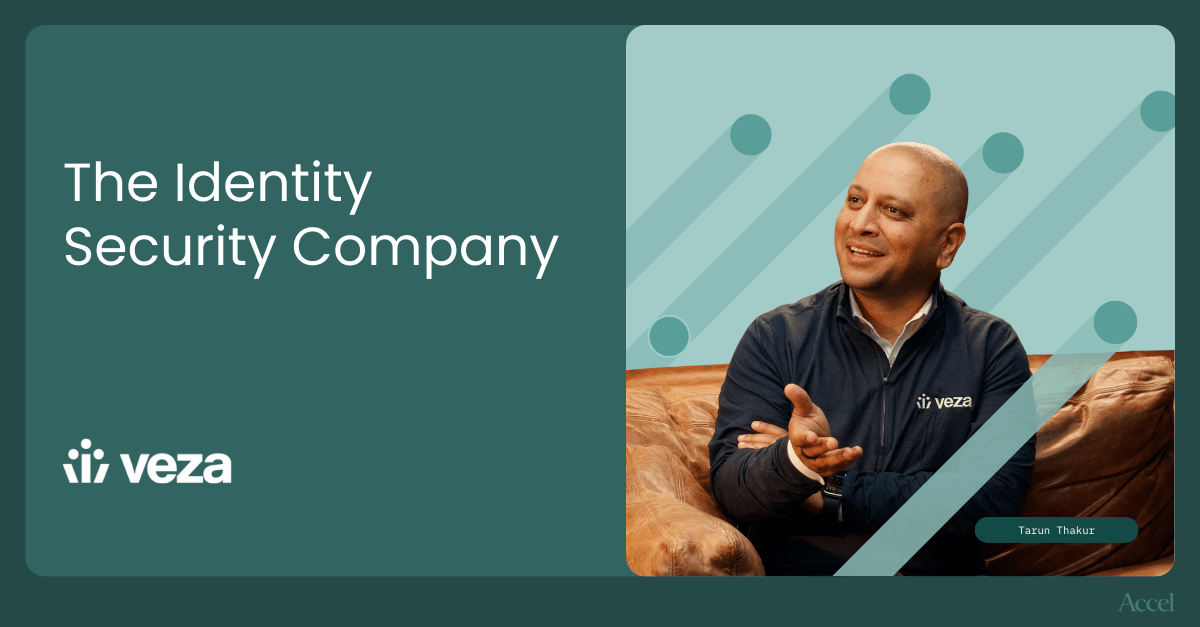

ServiceNow + Veza: Identity Security’s Next Chapter

December 2, 2025

Accel News

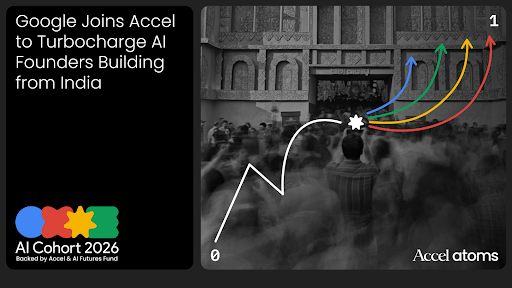

Google Joins Accel to Turbocharge AI Founders with Atoms AI Cohort 2026

November 24, 2025

Accel News

Welcome, AJ Tennant!

November 20, 2025

Portfolio News

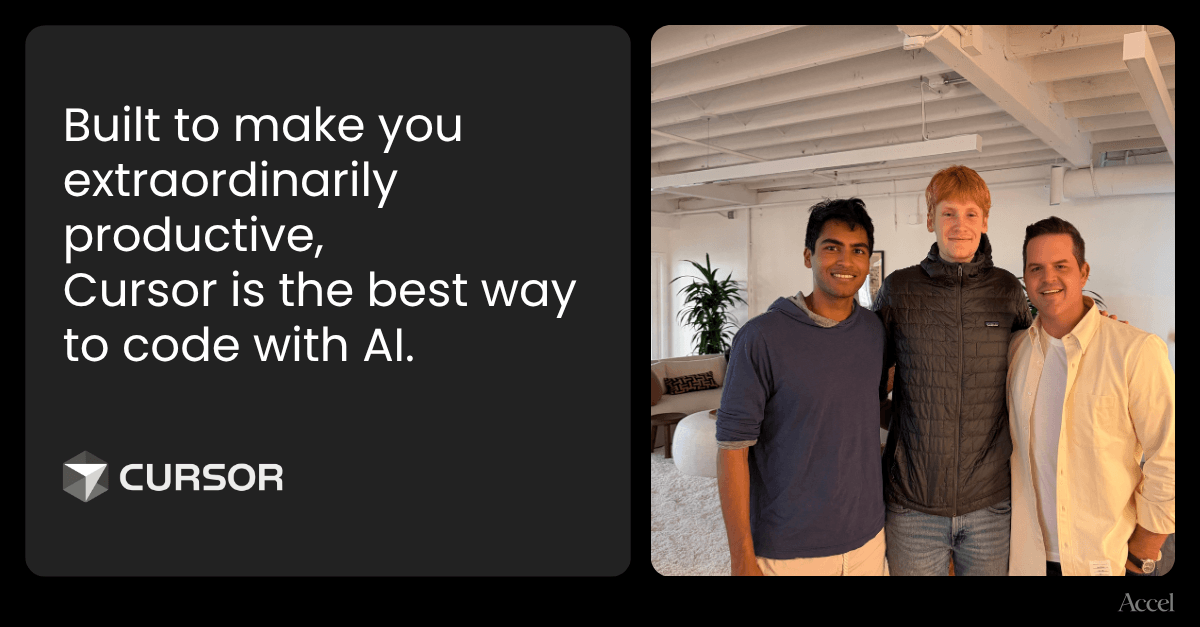

Our Series D in Cursor: Pushing the Frontier of AI Forward

November 13, 2025

Insights

Accel 2025 Globalscape: Race for compute

November 12, 2025

Portfolio News

Our Investment in Code Metal: AI Development for Hardware, Defense, and Regulated Industries

November 12, 2025

Portfolio News

Accel Leads VoidZero’s Series A: Revolutionizing JavaScript with a Unified Toolkit

November 5, 2025

Portfolio News

Restoring People’s Faith in Local Government: Our Seed Investment in Kaizen

October 30, 2025

Portfolio News

Leading Seezo’s Seed Round: Scaling Secure Design for Modern Engineering Teams

October 28, 2025

Portfolio News

Creating the Standard for Longevity: Our Seed Investment in Generation Lab

October 22, 2025

Portfolio News

Clove: Building the Financial Institution for a New Generation

October 14, 2025

Portfolio News

Our Investment in Flint: Marketing Superhuman-as-a-Service

October 14, 2025

Portfolio News

Our Investment in n8n: The AI Platform for Automation

October 9, 2025

Portfolio News

Our Investment in Kernel: The Best Browser Infrastructure for Agents

October 9, 2025

Portfolio News

The case for a universal health companion: Our investment in August AI

October 6, 2025

Portfolio News

Supabase’s Series E: An Era-Defining Database

October 3, 2025

Portfolio News

Our Series F Investment in Vercel: Building at the Speed of Ideas

September 30, 2025

Portfolio News

Polars: Transforming Data Processing on Modern Hardware

September 29, 2025

Portfolio News

Backing Rocket and the Shift to Vibe Solutioning

September 23, 2025